*For everyone’s safety we take phone appointments as well as in-person appointments*

Menu

How to Sell Your Home Before Foreclosure in PA

Questions Covered in This Article

Nobody wants to face foreclosure. Even in their toughest financial straits, the last thing anyone wants to do is give up their property.

However, foreclosure doesn’t have to mean completely giving up your choice in the matter.

If you’ve come to terms with losing your home, you can always choose to sell your home pre-foreclosure. By doing so, you can come up with the funds to avoid losing all of your property and save time.

Here’s everything you need to know about foreclosure in Pennsylvania and how to get ahead of it by selling your house.

Foreclosure is the legal process in which a lender takes possession of a mortgaged property in order to recover a loaned amount. This happens when a person fails or is unable to make payments on their mortgage.

Despite how common it is, not many people are aware of its actual definition.

There are many reasons that might lead to a foreclosure. Maybe you receive property in a will and can’t afford to pay for it. Or perhaps a nasty divorce has you struggling to make payments.

Once the process begins, the owner loses all rights to their property. However, this doesn’t include any free-standing appliances, furniture, and personal belongings. The property then goes to a foreclosure auction for sale at a lower sale price.

Pennsylvania Foreclosure Laws

When a person gets a loan to buy residential real estate, they have to sign a mortgage. A mortgage is a document giving the lender security in the property in the case of a failure to repay that loan.

Foreclosure in Pennsylvania starts when a person misses multiple payments and receives a breach letter from the lender. The breach letter is a notification that the loan is in default. If no response is given, then the lender moves forward with the foreclosure proceedings.

The lender files a lawsuit in court in order to foreclose. If you respond to the lawsuit, the case goes through the litigation process. It’s up to the judge to give the lender permission to hold a foreclosure sale if you’re proven guilty.

When Does Foreclosure Begin?

According to federal law, a loan provider can’t foreclose on a person unless they’re more than 120 days past due on their payments. However, the process can take as long as 200 or more days to conclude.

Tenants must be given a minimum of 90 days’ notice. You may also be allowed to stay until the end of your lease.

Can You Sell a Home in Foreclosure?

Until the bank officially takes possession of your home, you can try to sell your home pre-foreclosure to settle your debts.

Pre-foreclosure refers to the time period when a lender issues a notice of default but you’re still allowed to stay in the home.

You can ask the lender to postpone a foreclosure auction for a chance to find a buyer. Although you still lose your house, you end up saving your credit from damage.

Alternatively, some lenders agree to a short sale, where you sell your home for less than the owed amount. This type of deal is completely up to the lender’s discretion.

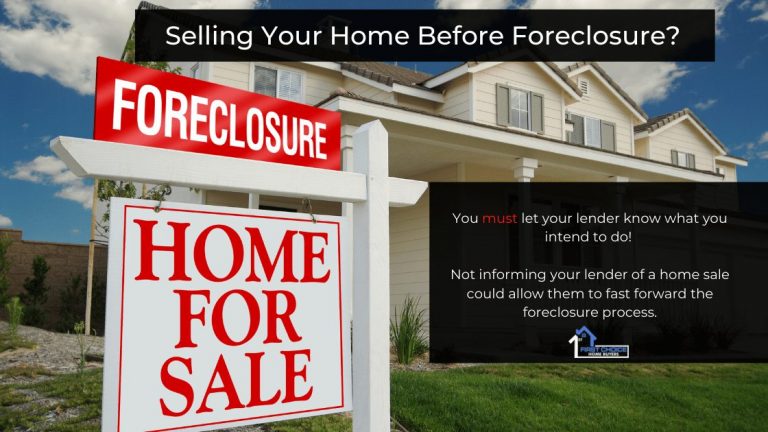

How to Sell Your Home Before Foreclosure

First and foremost, you have to let your lender know what you intend to do. Not informing your lender of a home sale could allow them to fast forward the foreclosure process.

Once you have their permission, you can get together with a realtor to start the process. This is a good option if you want to postpone the foreclosure process and save your credit score from further damage.

You may find your house hard to sell for a number of different factors, such as a tax lien. A tax lien secures the government’s interest in your property as a result of ongoing tax debt.

After a purchase offer has been made, you’ll inform your lender. If there are any tax liens on the house, you can’t transfer the title over. You need to clear them before closing a sale.

Although a tax lien stops you from selling a house, it doesn’t stop the mortgage lender from foreclosing on you. As such, it’s in your best interest to settle any tax debt before attempting to sell your property.

A designated settlement agent will take the loan balance and arrange for the payoff after a sale is finalized. Since the foreclosure process was never completed, you’ll have a better chance of financial recovery moving forward.

How to Prevent Foreclosure

A big part of preventing foreclosure is managing your finances before you miss too many payments.

Gather all of your documents, such as copies of your mortgage, monthly billing statements, and insurance information. It’ll help when you’re prioritizing the bigger issues to deal with.

Contact your servicer if you’ve missed a payment to see if you qualify for some kind of loss mitigation option. Loan modification helps you change the terms of your loan. Forbearance agreements allow you to reduce your payments until your finances are in better shape.

Worst comes to worst, a foreclosure moratorium can delay the process for up to 120 days. This is when a lender freezes foreclosure activities for some reason. Most recently, there was a foreclosure moratorium placed by the federal government in early 2021 due to the coronavirus outbreak.

Missing out on a couple of payments doesn’t mean you’re deep in a hole without a way out. Even though you may lose your home, you can at least get ahead of it by selling the property before you lose all rights to it.

If you’re facing foreclosure in Pennsylvania and need help selling, reach out to First Choice Home Buyers. We’re a local home buying company that offers cash offers for your home. We’ve helped home owners in Harrisburg, York, ( and York County), Hershey, Lancaster County, and the surrounding areas.

Contact us today to learn more and get your no-obligation cash offer.